In the realm of employee incentives and rewards, stock options have gained immense popularity. Of the many types of stock options plans available, companies are now preferring the Employees Welfare Trust (“Trust”) structure for issuing stock options instead of direct options from the pool.

Under the Trust structure, the company establishes an Employee Welfare Trust to implement a stock option plan. It is important to recognize that a Trust should not be considered as a legal entity but rather as an extension of the company that holds shares on behalf of the employees. Ideally, the Trust must maintain

a schedule setting out the shares held and the details of beneficial interest holders.

ESOP Trust as a Concept

A Trust is a legal set up that a company creates for the purpose of administering and governing stock options. Under this structure, the company transfers or issues new shares to the Trust. The Trust will then assign only the beneficial and economic ownership of shares to the employees on exercise of options while the legal ownership remains with the Trust. Economic benefit here means the right to receive dividend and other monetary rights that come with being the shareholders of the company.

Parties of a Trust

- TRUSTEE : Any person designated to manage the assets, funds, operations, and finances of the Trust. A Trustee can be anyone other than individuals who serve as the directors and key management personnel (along with their relatives) of a company including its holding and subsidiary company, or any person holding more than 10% of the paid-up share capital of the company.

- SETTLOR : The company that has created the Trust. Settlor is also known as Grantor or Trustor. As a practice founders are often the settlors.

- BENEFICIARY : The option holders- The employees of the company.

- PROTECTOR : Any person appointed to protect the interests of the beneficiaries. A key management personnel can be a ‘Protector’.

Steps to create an ESOP Trust

- Investor Protection Matters: Relevant shareholders approval must be sought for granting of stock options and adoption of the ESOP plan as part of the investor protection measures.

- Finalise the Trust Deed: The trust deed must be notarised on a stamp paper.

- Approval of the Board and shareholders: A board and shareholder meeting must be called for to implement and execute the trust deed, ESOP Pool, and ESOP Plan. If the company funds the Trust then a specific resolution must be passed in a general meeting to authorize the scheme for the provision of funds.

- Obtain PAN & and TAN: PAN and TAN must be obtained for the ESOP trust along with opening a bank account. Any contribution to be made by the settlor will be remitted to this bank account.

- Statutory filings: Statutory forms like MGT-14 must be filed with the ROC for the special resolution passed in the shareholders meeting.

- Settling of the Trust: Once the trust is created, shares are transferred to the trust. Trust can be settled in the following ways:

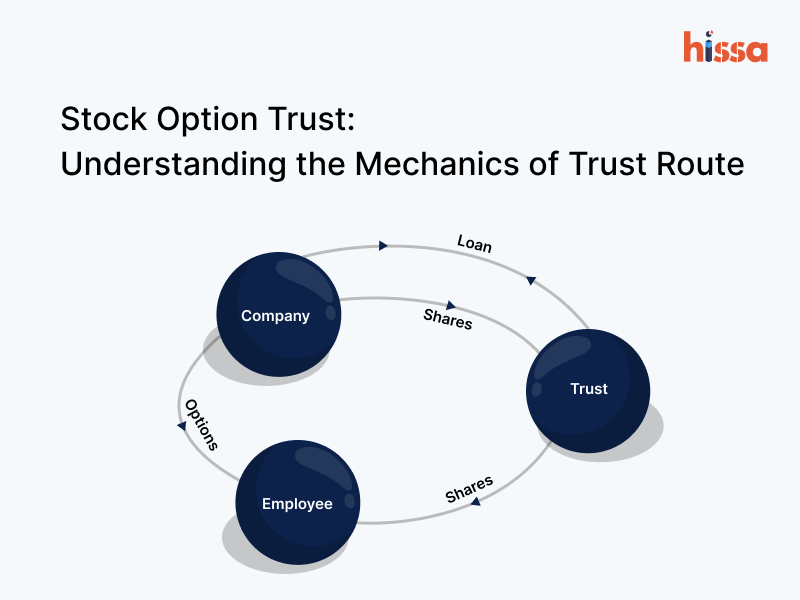

- Company grants a loan and the Trust subscribes for the shares in the company.

- Founders transfer their shares to the Trust

- Employees transfer shares(partially/fully) to the Trust.

ESOP Welfare Trust (EWT) Routes

Structure 1: Granting Options Following Trust Formation

- The company creates the trust to grant stock options to its employees. Company provides loans to the Trust to subscribe to purchase shares form founders or company.

- Founders transfer/ Company issues shares to the Trust. (This can also be done closer to exercise event).

- The company identifies the employees for stock option grants and calls a board meeting to seek approval of the grant. Company grants options to identified employees.

- Employees wishing to exercise options submit the exercise request to the Trust and pay the exercise/strike price.

- The company notes that the Trust will hold shares on behalf of the employees. The Trust provides a declaration to the employees for this purpose.

Structure 2- Creation of Trust After Grant and Exercise of Options

- The company identifies the employees for stock option grants and calls a board meeting to seek approval of the grant. Company grants options to identified employees.

- Employees wishing to exercise their vested options submit the exercise request to the company and pay the exercise/strike price.

- Company issues shares to the employees.

- Company creates a Trust.

- Employees transfer their shares to the Trust. Trust becomes the registered owner of shares and employee the beneficial owner.

What makes a Trust different from issuing options directly from the ESOP pool?

Under the direct route, stock options are directly granted to the employees of the company from the ESOP pool. The options vest and exercise is made in the employees’ names. Once exercised, the shares are allotted to the employees resulting in the employees getting a spot on the cap table of the company. The share certificates are also in the employees names.

In a Trust route, the employees are only the beneficial owner of shares and not the legal owner. This means, the shares are not held by the employees directly, the Trust holds the shares on behalf of the employees. Only the Trust name is reflected on the cap table of the company. The company can also decide whether to transfer/ issue the shares to the trust at the time of exercise of options by the employees or at the start.

What are the benefits of an ESOP Trust structure?

- The trustee being a professional body has an obligation to always act in the best interest of the employees. With the trustee managing the compliance requirements, employees who lack expertise in stock options can delegate the administration of their options to the Trust while enjoying the economic benefits.

- Since employees are not actually shareholders, termination of employment is relatively easy.

- If there are disputes among legal heirs, that will spill onto the cap table. In the case of a trust, it will only be a cash claim. Legal heirs will not get shareholder rights. Disputes will also not affect the Trust’s ability to transfer shares.

- Dilution of shares is already accounted for under the Trust, hence there is no new dilution when options are exercised.

- Multiple shareholder names on the cap table can be avoided. This helps the management to make decisions without having to take the consent of multiple shareholders. This also prevents employees from becoming shareholders and obtaining shareholder rights which could be problematic especially if the employee has moved to a competitor firm.

- Trust also ensures that all governance issues relating to stock options are substantially managed.

- In an M&A event, the Trust can transfer the shares without having to obtain the consent of Grantees. Sometimes, it may not be possible to track some of the shareholders – this happens when employees exercise Options and leave employment.

- Some investors insist that all shareholders are made parties to the shareholders agreement. The Trust can execute agreements.

Challenges of an ESOP Trust structure

- Companies may need to fund the ESOP Trust. The trust will then purchase the shares of the company.

- Setting up the Trust structure involves additional paperwork and compliances relating to setting up of the Trust, appointing trustees, obtaining PAN, TAN and so on.

- Shares held by a Trust may sometimes not be backed by options. In the event the options lapse or are forfeited for buyback, it leaves the Trust with shares that need to be liquidated. This can lead to additional compliances that the company has to follow.

- The company may transfer shares to the Trust who will in turn grant beneficial ownership to employees. This process can get complex. Along with this, the company must also manage audit and filings in relation to the Trust.

Tax implication of stock options under Trust

- On the company: There is no tax liability on the company. The company issues shares on exercise of options. Company deducts tax at source on the perquisite value of options exercised.

- On the Trust: The Trust only holds the shares on behalf of the employees. Any tax on Capital Gain is applicable at the time when the Trust transfers shares to the employees.

- On the employees: Difference between fair market value and exercise price is considered income of the employee. Tax is payable at the time of exercise on the difference amount (perquisite value). Capital gain tax is applicable at the time of sale of shares.

While companies can set up the stock option plan under the direct or trust route, lately there has been an increased usage of the trust structure grant options. While ESOP trusts offer significant advantages, careful planning is essential for success.