What exactly are Employee Stock Options?

Options are ‘rights’ granted to employees (and not obligations) to acquire the shares of the employer company at a fixed price (or Strike Price) against satisfaction of some conditions (Vesting Conditions). While the employee is not bound to exercise the Options, the company will be bound to honour the Grants as per its terms and conditions.

Why are they issued?

1. Ownership in the company: Employee ownership motivates the employees to participate in the growth of the company. This will therefore help attract and retain talent and incentivise employees to work towards the company’s growth. Ownership also helps create an emotional connection with the company further aligning the company’s goals with the individual goals. This gesture goes a long way in, motivating the personnel, team building, reducing attrition and improving the “employee brand” of the company.

2. Issue of grants attract talent: For companies that do not have the bandwidth to meet market compensation, startups may structure the package as a combination of components like joining bonus, annual pay, deferred pay and stock options. Stock options imbibe a feeling of belonging to the company and a willingness to go an extra mile for the benefit of the company as a whole.

How do stock options work? What are the different stages of stock options in the life-cycle of a plan?

Creation of a pool

An option pool is the pool that is earmarked for making grants. The pool is expressed as an absolute number. Since the pool dilutes shareholding, investors insist on creating the stock option pool before making the investment. The percentage of the ESOP pool usually ranges from 5% to 15% and is dependent on the nature of the business.

Adoption of a Plan

Grants may be made only under a stock option plan- ESOP, Trust or SAR. The company has to first create a plan. Creation of a plan will include setting the plan period, vesting, exercise parameters etc. Once the plan is created, employees are then assigned to the plan after which grants are made.

Making Grants

This is the act of telling an employee that he/she has received stock options. This is done by issuing a Grant Letter. The Grant Letter typically sets out the number of options, the vesting conditions and strike price. Other material aspects may also be set out.

Vesting of Grants

Vesting is the process by which a grantee’s right to acquire the underlying shares fructifies. Vesting is subject to satisfaction of some conditions called the vesting conditions.

The most common conditions for vesting are pure time-linked grants. The plans generally provide for a four-year vesting (with the grant vesting equally each year) with a one-year cliff. A cliff restricts the employees from leaving the company with shares after having worked for only a few months. options granted without cliff puts the company at a disadvantage because the replacement hired may also need to be compensated with stock options. After the first year, the practice is varied. Vesting may be monthly, quarterly or annual, with quarterly vesting being the most common practice.

In some cases, you may wish to introduce individual performance-based criteria for the options to vest. This can be the employees reaching a sales target, effective client engagement etc. The third condition can be event based. Here, options could be linked to the company achieving some revenue targets, profitability, etc.

Exercise

Exercise is the act of subscribing to or purchasing the shares. This involves sending a letter of exercise and executing documents that are required to be exercised. Once exercised, the company issues shares to the grantee and the grantee becomes a shareholder. If the plan is being administered by a trust, the trust transfers shares to the grantee.

The ESOP policy of the company is put to the real test at this stage. It involves a substantial cash outflow for the individuals. If they believe in the potential of the company to give an upside, they would go an extra mile to acquire shares of the company, despite the heavy cash outflow.

Exercise of shares is considered as a taxable event in India. The gains made on exercise are taxed as employment income for the grantee. An important point to note is that the individual has a right to exercise the grants or stock options; there is no obligation or compulsion to exercise the right.

Buy-back of Options

Companies may run option buy-back / surrender programmes for options. These programmes provide liquidity to employees.

Disposal of Shares

If options have been exercised, the final phase would be the sale of shares. The share sale may happen in four broad situations: (a) company facilitated acquisition of the shares by third parties, (b) company buy-back, (c) as part of the acquisition of the company and (d) sale by the Grantee post the IPO. Sometimes, grantees are able to sell to private buyers prior to a listing of the company’s shares.

What are the different kinds of stock option plans?

1. Employee Stock Ownership Plan(ESOP): ESOPs are intended to encourage employees to acquire ownership in the company. Under this Plan, employees have the option to purchase the company’s shares in the future at a fixed discounted price. This means, employees can convert their options to shares at a price lower than the existing value of shares, the difference being the reward for the employees.

2. Employee Stock Purchase Plan (ESPP): Employees have the right to purchase the shares of the company at a discounted value. In few companies, an agreed percentage of the employee’s salary is deducted which is then aggregated to buy the company’s stock on scheduled dates in the future. Company law, IT, FEMA, SEBI govern ESOP in India. ESPP is also relevant only for listed companies really. ESPP may be there when plans are implemented by trusts. In these scenarios they are no different from option plans.

3. Stock Appreciation Rights/Phantom Stock: In phantom grants (also called Stock Appreciation Rights), the employee gets the economic benefits associated with options but not the right to become a shareholder. The employee is entitled to the difference between the strike price and the fair value of the underlying shares (upon Vesting). In cash terms, it is identical to options. From the company’s perspective, the value of the vested phantom units has to be recorded as a cash liability on the books.

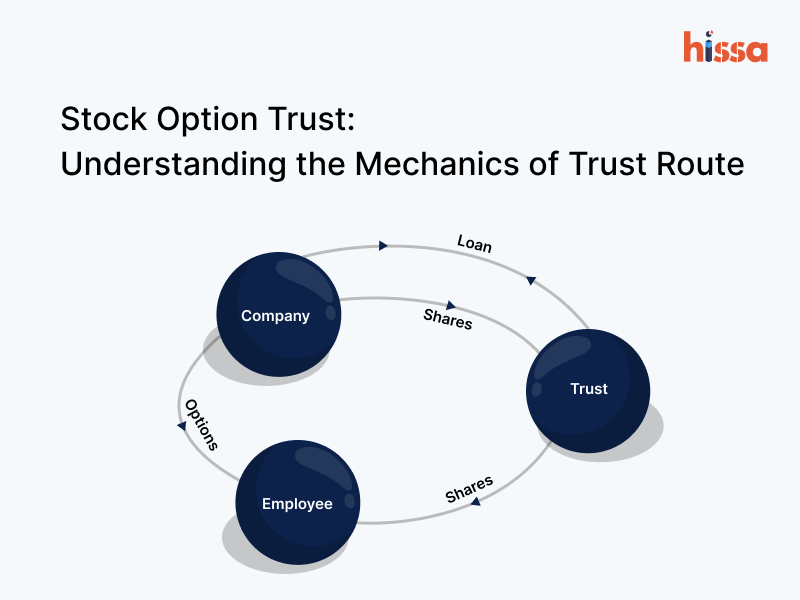

4. Trust: The company sets up a trust to whom legal ownership of shares is granted. The trust then grants beneficial ownership of the shares to the employees of the company. The trust here acts as an intermediary between the employees and the company to carry out transactions regarding options. On exercising stock options, employees are granted all economic benefits of ownership of shares like the right to receive dividend, vote etc., while legal ownership remains with the trust. In unlisted companies, the trust provides an exit mechanism to the grantees especially since there is no secondary market for sale of shares.

Is there any relaxation for ESOPs issued by start-ups?

The employer deducts TDS immediately on exercise of ESOPs. This may lead to a temporary liquidity crunch where the employee is required to pay for acquiring shares and also for the notional gain based on the FMV at the time of exercise.

To address this anomaly, certain eligible start-ups are entitled to defer their tax liability, i.e., tax liability in the year of exercise can be deferred up to the earlier of 4 years from the end of the year in which the ESOPs were exercised, the date of sale or the date of cessation of employment.

What regulations govern stock options in India?

Companies that have issued stock options are required to adhere to the laws generally applicable to a company as well as the laws specifically applicable to the issue of shares / stock options.

The applicability of laws and the manner / extent of applicability also depends on the structure of the stock options, the residential status of the employee and similar factors. If the employees are non-residents then FEMA regulations will need to be followed.

Likewise, the compliances may be lesser in implementing ESOPs under a direct route as compared to a trust route. From the employees’ perspective, the trust route provides an exit mechanism to employees of unlisted companies, where there is no open market for the disposal of shares. From the employers’ perspective, the management of the stock option plan is taken care of by an independent entity which implements the plan, communicates with the employees and addresses their queries and grievances. Further, the voting rights in respect of shares held by the ESOP Trust are exercised by the ESOP trustees and not individuals. This reduces the governance issues involved when shares are held by multiple individuals, especially those who are no longer present in India. Considering that the trust route offers greater commercial advantages over decision making in the company, a company may go ahead with the trust route.

Now, let’s look into the specific regulations governing stock options.

1. Corporate Law

- The Companies Act is one of the most important regulations governing the issue of stock options. Any company issuing stock options must comply with the provisions of the Companies Act, 2013 and the Companies (Share Capital and Debentures) Rules, 2014. Broadly, these provisions regulate:

- Whether an employee can be issued stock options – Generally, employees of the company or its holding or subsidiary companies can be granted stock options. An employee belonging to the promoter group or a director holding more than 10% of the share capital in the company cannot be granted the stock options (certain relaxations are provided to qualifying startups for 5 years from incorporation).

- Stock option structure including identification of employees or class of employees eligible for the offer, vesting conditions and timelines, exercise price and process, lock-in period post acquisition of shares and so on.

- Rights of the option holder before and after exercise – an option holder does not have a right to vote or receive dividend until the shares are actually issued upon exercise.

- Procedure for issue of stock options including preparation of the stock option plan, board approval, shareholders’ approval etc.

- Compliances after the issue of stock options – maintenance of the Register of Employee Stock Options, filings with the MCA, issue of share certificates to the shareholder upon exercise etc.

2. Accounting

- Issue of stock options entails a cost to the company and must be booked as an expense. Startups generally follow the iGAAP for accounting purposes. It provides guidance on the manner of accounting of the expense and the period of years for which the expense must be booked.

For instance, the cost of stock options is booked over the vesting period. The cost is arrived at based on the fair market value of shares of the company on the grant date.

3. Income Tax

From the company’s perspective:

The cost of stock options to be spread over the vesting period is a deductible expense for the company. The expense may be disallowed if it is not in accordance with the accounting guidelines applicable to the company.

The taxable value of stock options is considered as ‘perquisite’ for employees and is taxed as ‘Salaries’. The company must deduct tax on the perquisite value. In case of cash-settled SARs, tax is deducted before making the payment in case of SARs. When it comes to stock options, TDS on the notional perquisite value is deducted from the employee’s salary.

4. FEMA

An Indian company can issue stock options to non-residents. Non-residents may be employed by the company itself or by its overseas holding company, subsidiary company or a joint venture.

Issue of shares to a non-resident is regulated by Foreign Direct Investment Regulations under FEMA. The regulation provides for the sectoral caps to be adhered to by the company and seeking approval in certain cases, the price at which shares can be issued, reporting by the Indian company etc. For instance, the shares on exercise cannot be issued at a price lower than the fair market value of shares of the company, calculated as prescribed.

Practical issues may arise if the fair market value of the company at the date of exercise is substantially different from the value on the date of grant.

5. Other regulations

In addition to the above, there are other regulations like Stamp Duty and Contract Act governing the issue of stock options. The stock option agreement between the company, employees and the ESOP Trust (if any) must be in compliance with the Contract Act in order to be a valid contract.

The agreements and shares issued on exercise must be duly stamped by paying stamp duty at the applicable rates. Likewise, listed companies are also governed by SEBI guidelines on issue of stock options.

There is a web of regulations governing any stock option plan. A company may set up an in-house compliance team or outsource the compliance to independent practitioners. Alternatively, there are certain platforms which can help a company in managing the ESOP process, the cap table and future planning.

What are the most common terms that the management has to consider when setting up an ESOP plan?

Since ESOP involves a number of processes from designing to governance, the following list of questions will help you structure a basic stock option plan. It has been broken down into 3 sections:

Instrument Related:

- What is the maximum number of stock options that can be granted to an employee?

- What should be the vesting conditions?- Vesting period, cliff, interval.

- What should be the exercise price and exercise period?

- How can stock options be exercised? Can options be exercised multiple times in a given year?

- Should this be a cash or non-cash exercise?

- How long should the exercise window remain open?

- How will the stock options be valued?

Employee Related:

- Who are the eligible employees? What is the criteria for an employee to become eligible to receive stock options?

- How many employees will be covered under the stock option plan?

- In an event of termination, death, incapacity of an employee, how will the stock options be treated?

- Who is liable to pay tax pursuant to exercising the options?

ESOP governance:

- What internal policies/conditions need to be complied with before granting stock options?

- What documents need to be in place in connection to stock options?

- What should be the percentage of the stock option pool?

- How will the stock option plan be implemented?

- Who is responsible for managing the stock options?

- What are the disclosure requirements of the stock option plan?

- How are the unvested options treated?

- How should stock options be treated in an event of merger/amalgamation/ liquidation of the company?

Over the years, stock options have proven to be a good retention tool. With many companies providing liquidity programmes, employees have been able to earn good returns in a short period.